Economic policies are diverging in the developed world as deflation looms

CENTRAL banks in the developed world are no longer acting in tandem. When the financial crisis broke in 2007-08, most banks eased monetary policy significantly. But in late October, two days after the Federal Reserve ceased its third programme of asset purchases, the Bank of Japan stepped up its bond-buying. This divergence seems likely to have a big effect in the medium term, not least in the currency markets.The Bank of Japan said it was expanding its programme of asset purchases (known as quantitative easing, or QE) from ¥60-70 trillion to ¥80 trillion ($700 billion) a year. Its aim is to ward off deflation, a persistent problem over the past 20 years. The Tokyo stockmarket jumped sharply on the news but the biggest economic impact may be on the exchange rate. The yen fell more than 2% against the dollar on the day of the announcement—a big move by currency-market standards—and hit a seven-year low against the greenback on November 3rd.

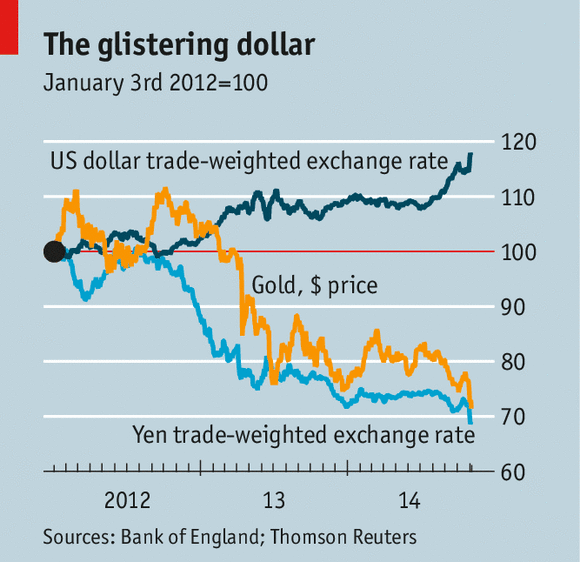

The dollar has been gaining ground more broadly in recent months (see chart). This seems largely due to America’s relatively strong recovery (by the rich world’s feeble standards) and the perception that this will lead the Fed to raise interest rates sooner than other central banks. The market’s view of when the first rate rise will come has varied a lot, but the Fed’s latest statement was seen as fairly hawkish; the current consensus is some time in November or December next year. Those investors who like to play the “carry trade”—borrowing money in a low-yielding currency to invest in a higher-yielding one—can already exploit the big gap in yields between Treasury bonds and German or Japanese government debt. Higher short-term interest rates will give them another incentive to buy the dollar.

For Japan, a weaker yen is broadly positive. It pushes up inflation by raising the cost of imports and boosts the prospects of Japanese exporters by making them more competitive in global markets. Exchange rates are a zero-sum game, however: if Japanese exporters gain market share, some other country’s exporters must lose it. And if competition from Japan forces producers in other countries to lower their prices, the effect could be to export deflation to the rest of the world.

Over the past 12 months, for example, the yuan has risen nearly 15% against the yen. That has put pressure on Chinese manufacturers to cut prices; the Chinese producer-price index has fallen for 30 consecutive months, the longest decline since the late 1990s. In turn, that puts further downward pressure on American inflation; since 1995, there has been a 70% correlation between Chinese producer prices and American consumer prices, according to Deutsche Bank.

If other central banks in the developed world respond to the yen depreciation by loosening monetary policy, then the net effect on economic growth would be positive. But the Fed and the Bank of England have stopped easing and the European Central Bank seems reluctant to adopt QE. The extra burst of Japanese QE may only offset a planned rise in the consumption tax, so the net effect on global demand could be zero.

A further sign of the growing worries about deflation can be seen in the gold price. Gold’s decline was not halted by the Bank of Japan’s move; it even accelerated. Yet when QE was first adopted, many investors piled into gold as a hedge against the rapid inflation they thought it would inevitably unleash. As it turns out, that dog has not even whimpered, let alone barked. Even the argument that the inflationary impact of QE has shown up in asset prices has been of little comfort to the gold bugs. Equities and corporate bonds have enjoyed much higher returns than gold itself. The S&P 500 index has almost doubled, in gold terms, since 2009.

The most bull(ion)ish arguments in favour of gold hinged on the notion that the dollar would collapse due to the toxic combination of massive government debts and QE. Gold is seen by many as the dollar’s main competitor as the world’s reserve asset. So the dollar’s resurgence undermines another pillar of the case for gold. More than $1.3 billion was withdrawn from precious metal funds in October, according to Bloomberg.

Add together a weak gold price, falling commodity prices, low government-bond yields and downward revisions to growth forecasts and one has a recipe for deflation. That is the last thing that countries with high debt burdens need. Small wonder if governments decide it is every man for himself.

Comments

Post a Comment